Having a Good Time at HGTY?

Having a Good Time at HGTY?

Natural Aspiration 14: Sherman Peaks Under the Hood of Hagerty's Transformation

When did you first become familiar with Hagerty, the specialty insurer headquartered in Traverse City, Michigan?

When you sought insurance coverage for your wooden boat? Few are aware, but that’s how the business began.

Or, similarly, when you needed insurance coverage for your classic or specialty vehicle?

Maybe a television commercial on Speedvision (or a successor entity)?

Or perhaps more recently, when your favorite automotive writer, YouTuber, podcaster, or other media personality began creating content on one of Hagerty’s platforms?

I am in the first category; my father at one point insured his collection of wooden boats with Hagerty. If you are in the fourth category, your familiarity with the company helps justify the specialty insurer’s recent spending spree.

In 2000, McKeel Hagerty became CEO of the company his parents founded in 1984. Recognizing both that the supply of classic cars, to say nothing of wooden boats, was inherently limited and that the automotive enthusiast hobby would likely encounter existential threats in the future, McKeel sought to raise the profile of his family’s business in the 2010s (emphasis mine throughout):

“Our mission as a business is to save driving and car culture for future generations,” said McKeel Hagerty, CEO. “We’re not just in the insurance business. We certainly started in insurance, and we’ll certainly continue doing that and we’ll do a lot more of it.”

“But it’s all this idea of an automotive lifestyle: events, even — potentially — membership physical locations someday. All of our media efforts will start expanding, and the business will expand even faster,” Hagerty said.

Some of the growth will be made possible by an infusion of cash from Markel Corp., a multi-national holding company for insurance, reinsurance and investment operations. The company recently paid $212.5 million to acquire a 25 percent stake in Hagerty.

The Traverse City Record-Eagle published this article in September 2019; the minority investment from Markel implied a valuation of $850 million.

“It was really a match made in heaven,” said Hagerty. “We just invited them into the owner group and now we’re ready to continue growing the business as we planned.”

Much of that growth involves the Hagerty Drivers Club, which offers members-only events, a magazine, automotive discounts, roadside service, membership in a historic vehicle association and access to an automotive help desk.

“The Drivers Club is our big evolution as a business,” Hagerty said. “It went from kind of a sideline to the headline.”

More than 1.4 million people now belong to the Hagerty Drivers Club. The company aims to increase membership. Business growth requires capital. The Markel deal offered a large chunk of capital.

“Markel is a really great long-term partner with another side of our business, which is they’re a risk-taking partner with us,” Hagerty said. “We’re a risk-taking business, so we actually don’t just sell insurance, we actually bear some of that risk. So we’ll have additional capital to be able to do even more.”

I am a Hagerty Drivers Club member, I think. I am almost certain that I was a member at one point. I found the “privileges” on offer of such little value that I am unaware as to whether I am still entitled to them; at any rate, I have never used - or valued - them.

The deal began taking shape almost a year ago. Terms were solidified last winter.

“It took forever to close,” said Hagerty. “Because we’re in the risk-taking business, and because of our reinsurance company in Bermuda, there was a lot of regulatory scrutiny — as there should be. Between Bermuda and Missouri and a couple of other states that were involved, it took a lot longer.”

Selling a stake in the company was the best way to raise money for expansion.

“Because of the regulated nature of the business, you have to use actual capital,” said Hagerty.

The ownership stake Markel purchased doesn’t include any kind of control in the Traverse City company.

Hagerty employs 1,200 people, more than two-thirds of them in Traverse City.

Efforts to expand its Drivers Club drove Hagerty earlier this year to buy a collector car insurance program from Kemper.

“This is potentially 50,000 to 60,000 additional members who will be, now, part of the Driver’s Club and be able to help us in our purpose of saving driving,” he said of that purchase. “Members in the Driver’s Club is our ultimate goal. Insurance is wonderful to help us get there.”

In early 2016, Hagerty poached Larry Webster from Road & Track, where he had served as Editor in Chief since 2012. Webster would “oversee Hagerty’s print and online media strategy and engagement.” He then recruited ex-R&T personnel, including Sam Smith and Jack Baruth, to join him. The appeal of writing for Hagerty versus one of the traditional “buff books” was obvious. Whereas the legacy elements of automotive media - i.e., printed magazines with websites mirroring (some of) their content - were in terminal decline due to dwindling relevance, static at best circulation, and declining advertising revenue, Hagerty was not reliant on the skimpy revenue streams impacting the industry at large: Ads, subs, and newsstand purchases. Rather, Hagerty’s media efforts were a billboard for Hagerty itself, and the broader Hagerty business enjoyed a robust stream of insurance premium revenue to fund the media side of the house.

The brand building exercises continued.

In early 2021, Hagerty announced a revamped YouTube presence, which would feature both legacy Hagerty content - e.g., Redline Rebuild and Chip Foose Draws a Car - as well as new shows designed to appeal to new (read: younger) audiences; the first “season” of new shows featured some big names (emphasis added) and included:

Next Big Thing with Magnus Walker -A 6-part series, where Magnus Walker, famed Urban Outlaw, dives into affordable and unappreciated classics, and discovers the Next Big Thing.

Rated – A professional driver and a seasoned journalist head to the track with the most exciting new cars, taking a deep-dive approach to fully understand what they offer – often with a few disagreements along the way.

Jason Cammisa On The Icons – Untold stories of automotive legends: a visually stimulating and entertaining wiki video series on why certain automotive icons become legends.

Know It All (Jason Cammisa) – A short-form, humorous, quick-take on any technical concept pertaining to owning, driving, engineering, or talking about cars.

Revelations (Jason Cammisa) – A 20-minute, broadcast-quality visual and acoustic review of the most important cars of all time.

Rad Ventures – Ryan Symancek revisits the icons of the 80s and 90s. In this 4-episode mini-series, he examines standard variations of rad-era classics, and then puts them head-to-head with their modern equivalent.

Buyers Guide – A reboot of a classic Hagerty series, where the most desirable vintage cars are brought to life. Hagerty experts give value information and helpful advice to anyone looking to purchase them.

Not all of these shows found success, and Hagerty has modified their content orders in subsequent seasons. For example, Hagerty hired Matt Farah to present a show entitled Modified, in which he drove, uh, modified cars. While I enjoyed the videos - I am generally a fan of Matt’s content - apparently an insufficient number of viewers felt the same way, and Farah mentioned on his podcast that Hagerty had declined to renew Modified for an additional season.

The biggest, most enduring names on Hagerty’s YouTube channel have been Magnus Walker and Jason Cammisa. Magnus began with a series called The Next Big Thing, and his most recent effort was The Big Thing. The former series focused on collectible cars on the cusp of greater renown (and value), whereas the latter featured bona fide objects of wish fulfillment dreams (Ferrari F40, Mercedes Gullwing, and so on). I understand that the “Urban Outlaw” does not currently feature in Hagerty’s go-forward content strategy.

The final episode of The Big Thing went live on August 12, 2022. Just eleven days later, Magnus Walker’s girlfriend - Bloomberg’s automotive lifestyle correspondent Hannah Elliott - wondered aloud while attending Monterey Car Week as the beneficiary of various automotive manufacturers’ financial largesse:

Did these conflicts of interest exist while Magnus was working for Hagerty, or did they only begin during the eleven-day interim period? We’ll return to Broad Arrow Group - Hagerty’s recent automotive auction house acquisition - shortly.

A final note on Ms. Elliott: While her reporting is important to luxury and aspirational brands given Bloomberg’s readership demographics - a former luxury brand PR operative informed me that a negative review from Hannah augured poorly for a luxury car’s market prospects (to say nothing of a PR flack’s ongoing employment) - there are some blind spots in her industry knowledge. She once inadvertently featured a post from the satirical, anonymous automotive industry insider Instagram account “Woke Wheels” in a Bloomberg article covering controversial developments at Petrolicious. In other words, she got Punk’d.

Meanwhile, Jason Cammisa’s galaxy of content continues to expand: There are 26 episodes of Revelations (to date), and Jason’s most ambitious, cinematic content appears on the Icons playlist; he is now also filming drag races, à la the popular UK channel carwow. Cammisa’s Know It All videos appear to be deceased, however. Despite his tremendous popularity with viewers, some of Cammisa’s fellow content creators are not fans of his output:

In addition to the content offensive, Hagerty has been an active acquiror of various automotive lifestyle events and has undertaken other initiatives to expand its brand; here’s a non-exhaustive roster of recent moves and pertinent news updates:

6/23/21 - Hagerty announces its acquisition of the Amelia Island Concours d’Elegance; this “follows Hagerty’s recent acquisitions of other premiere automotive events, including the Concours d’Elegance of America, the California Mille and the Greenwich Concours d’Elegance.”

7/27/21 - Hagerty announces opening of “its next premium clubhouse and car storage facility, Hagerty Garage + Social Toronto, which follows the openings of clubhouse locations in Chicago, Delray Beach and New York.”

8/10/21 - State Farm, the nation’s largest insurer of private passenger vehicles, announces it is “collaborating with Hagerty to introduce new coverage for classic vehicles beginning in 2022.”

8/16/21 - Hagerty announces its acquisition of McCall’s Motorworks Revival, the annual Monterey Car Week kickoff party that takes place on Wednesday evening at the Monterey Jet Center; Hagerty later rebranded the event as “Motorlux.”

8/18/21 - Hagerty and Aldel Financial announce special purpose acquisition company (SPAC) transaction, whereby Hagerty became publicly traded on the New York Stock Exchange (NYSE); I will cover the SPAC deal in greater detail later in this piece.

12/3/21 - SPAC deal completed; Hagerty begins trading on NYSE under ticker HGTY.

1/10/22 - Hagerty announces strategic investment in Broad Arrow, “accelerat[ing] marketplace strategy.”

3/9/22 - Hagerty announces its acquisition of RADwood, “an event brand devoted to celebrating the ‘80s and ‘90s automotive lifestyle.” Art Cervantes and Warren Madsen, two of RADwood’s founders, joined Hagerty in the aftermath of the acquisition. Bradley Brownell, another RADwood founder, did not join Hagerty; Brownell, recall, is the author of the above quoted tweet in which he claims that “nobody prays at the altar of toxic masculinity more diligently than Jason Cammisa,” Hagerty’s video superstar.

3/24/22 - Hagerty announces 2021 financial results; highlights include:

Total Revenue growth of 24% Year-over-Year (YoY) to $619.1 million

Written Premium growth of 17% YoY to $674.3 million

“Total Active Members” growth of 13% YoY to 2.4 million

4/14/22 - Hagerty announces its acquisition of Speed Digital, “an industry leading provider of cloud-based technology solutions for dealers, auction houses, collectors and enthusiasts.”

5/9/22 - Hagerty announces 2022 Q1 financial results; highlights include:

Total Revenue growth of 30% YoY to $167.8 million

Written Premium growth of 16% YoY to $154.8 million

“Total Active Members” growth of 11% YoY to 2.5 million

8/10/22 - Hagerty announces 2022 Q2 financial results; highlights include:

Total Revenue growth of 23% YoY to $206.0 million

Written Premium growth of 14% YoY to $237.7 million

“Total Active Members” growth of 9% YoY to 2.5 million

8/10/22 - Hagerty announces it has entered into a Definitive Agreement to acquire all outstanding shares of Broad Arrow, “which specializes in the transactional segments of the collector car market.”

“Earlier this year, Hagerty acquired approximately 40 percent equity ownership in Broad Arrow as a centerpiece of its automotive Marketplace strategy, designed to provide consumers new trust-based platforms for buying, selling and financing collectible cars. Hagerty is now acquiring the remaining 60 percent of Broad Arrow for $64.8 million in an all-stock transaction, with an expected closing date of August 16, 2022.”

The announced transaction terms imply an aggregate valuation of $108.0 million for Broad Arrow.

There are several methods by which a company may become publicly traded; the classic pathway is an Initial Public Offering (IPO), a popular COVID-era alternative was a merger with a Special Purpose Acquisition Company (SPAC), and a third, rarer option is a Direct Listing, which is sometimes referred to as a Direct Public Offering (DPO).

The IPO process is costly, laborious, and protracted. The SPAC alternative is typically quicker and can entail lower fees and costs.

In a SPAC process, a sponsor raises money from the public market through an IPO. The sponsor is typically a seasoned, prominent investor with a proven track record of value creation; this sort of resume, is not, however, required of sponsors. The SPAC IPO process is simplified and streamlined, because the entity that becomes public is a “blank check” company with no assets or history that will subsequently be hunting for a suitable acquisition target. There are myriad benefits to the company that sells to the SPAC: Less stringent public disclosure requirements, no juicy underwriting fees for investment bankers, and the aforementioned quicker timeline. There is a major benefit for the sponsor arranging the SPAC: Sponsors receive a “promote” fee for sponsoring the SPAC, and this is usually 20% of the shares of the SPAC. Not for nothing are SPACs often viewed as get rich quick schemes. The lack of disclosure surrounding the SPAC’s ultimate target potentially underserves investors.

Robert Kauffman was the sponsor of the Aldel Financial Inc. SPAC, which announced its acquisition of Hagerty in August 2021. Kauffman was a co-founder, principal and member of the board of directors of Fortress Investment Group from its founding in 1998 until his retirement in 2012, and he is an advisory board member of McLaren Racing, as well as a co-owner of Chip Ganassi Racing. He also owns RK Motors, “a leading restorer, re-seller and provider of classic cars.” Further, Kauffman also held an ownership position in Speed Digital, which Hagerty later acquired in 2022; I would view this as a potential conflict of interest.

As an interesting aside, I have it on very good - but not absolutely ironclad - authority that Kauffman pursued an equity investment in Carter Bank & Trust, the community bank with intimate ties to coal mining (former) billionaire, Greenbrier resort-owning, West Virginia Governor Jim Justice. The now-insolvent, Softbank-backed supply chain finance company Greensill Capital was also involved in Justice’s financial downfall - exciting!

For all his financial nous, Kauffman is perhaps best known for this incident:

From Motor Sport Magazine’s race report (emphasis mine):

But Mike Rockenfeller’s accident in the number one Audi at 10.40pm was far from blameless. At the Mulsanne kink ‘Rocky’ came up behind the AF Corse Ferrari of Robert Kauffman and went to pass it on the right. As he drew alongside at over 200mph Kauffman inexplicably drifted into the path of the Audi and clipped the back of it. The R18 speared left and hit the barrier almost at full tilt. By the time it came to a halt only the tub of the car remained, but after spending a night in hospital as a precaution, Rockenfeller was released unharmed. Remarkable. Kauffman was consequently withdrawn from the race by the ACO.

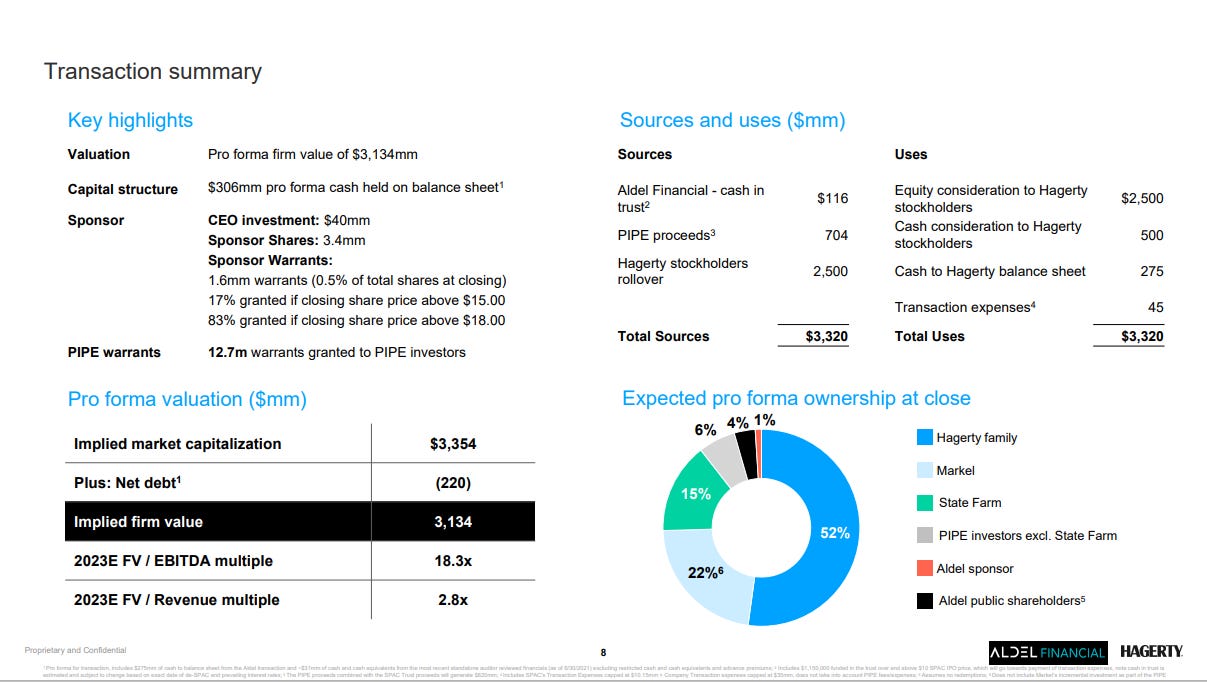

The Investor Presentation selling the merits of the SPAC is illustrative:

The transaction valued Hagerty at $3.1 billion on a pro forma basis and included a $704 million fully committed private investment in public equity (PIPE) led by strategic partner State Farm and existing investor Markel Corporation; other participants included “leading institutional and private investors.” The transaction was expected to deliver up to $820 million of gross proceeds to the combined company, including the contribution of up to $116 million of cash held in Aldel’s trust account from its initial public offering in April 2021 (assuming no redemptions). Hagerty later specified that net proceeds of approximately $265 million would be used to “advance Hagerty’s strategic growth opportunities, including digital innovation initiatives.”

Aldel’s IPO priced at $10.00 per share, which is the convention for SPACs. Post-transaction close, HGTY shares began trading on 12/3/21 and closed on 10/14/22 at $8.91 per share, representing a market cap of just under $3.0 billion.

I was a bit perplexed when I read about Hagerty’s acquisition of the outstanding shares of Broad Arrow; let’s delve into the auction house’s brief history (emphasis mine throughout):

12/6/21 - Broad Arrow announces its formation:

“A group of industry veterans with over 100 years of combined experience have launched a new company in the collector car industry.”

Broad Arrow “plans to develop a portfolio of businesses and brands to address the needs of various segments of the collector car market, including auctions, private sales, and financial services.”

Broad Arrow “is led by Chief Executive Officer Kenneth Ahn, who most recently served as President of RM Sotheby’s from 2016 to 2021.”

1/10/22 - Hagerty announces strategic investment in Broad Arrow:

“Central to the joint venture is Hagerty’s employment of four key Broad Arrow Group founders: Kenneth Ahn, Alain Squindo, Ian Kelleher and Mike Mortorano. In addition to his role as the CEO of Broad Arrow Group, Kenneth Ahn joins Hagerty as the President of Marketplace.”

2/9/22 - Broad Arrow announces launch of Broad Arrow Capital, “a dedicated financing business” that “will provide tailored financing solutions to eligible high net worth individuals, accredited investors, and businesses, secured by their collector cars in the United States, United Kingdom, and Europe.” The press release goes on to specify:

“Broad Arrow Capital is led by a team with over 60 combined years of finance, banking, legal, and collector car industry experience. Both Kenneth Ahn and Karsten Le Blanc previously founded and ran some of the most respected collector car financing businesses in the North America and the UK. They are joined by Mike Mortorano who will provide legal and administrative expertise.”

“The company will primarily focus on providing loans greater than $150,000 / £100,000 / €125,000, secured by collector cars.”

It’s my understanding that Broad Arrow’s financing arm was perceived as a key driver of value for the nascent auction house; bear in mind the staggering difference between the effective Fed Funds Rate in February 2022 versus October 2022. Moreover, the market anticipates further Fed rate hikes.

A non-bank lender like Broad Arrow is typically funded with warehouse lines from large banks; the typical non-bank finance company’s cost of (debt) capital is usually expressed as the Wall Street Journal (WSJ) Prime Rate plus a floating margin above the Prime Rate (usually at least 150 basis points, and potentially more).

At press time, the WSJ Prime Rate is 6.25%; so, e.g., a non-bank lender’s cost of funds would be 6.25% + 1.50% (if not more), or 7.75% (at a minimum) in total. In this example, a finance company would almost certainly have to charge double-digit interest rates to borrowers to earn an acceptable net interest margin.

“High net worth individuals, accredited investors, and businesses” won’t want to pay double-digit rates to finance collectible cars; here’s an illustration of superior borrower economics:

Let’s say you have a brokerage account with Charles Schwab, as I do, and you’d like to borrow against your portfolio to finance the purchase of a $1 million - or more - automobile:

Schwab, which owns a subsidiary bank whose 2022 Q2 cost of funds was just over 10 basis points, will advance you a loan at SOFR - that’s the Secured Overnight Financing Rate, the replacement for LIBOR - plus 2.40%, at press time.

SOFR is currently 3.04%; 3.04% + 2.40% is 5.44%, which is materially less than what I estimate is Broad Arrow’s cost of funds, to say nothing of the ultimate rate offered to borrowers!

Would you rather pay 5.44% to finance a $1.0 million - or more - collector car or perhaps double that rate?

3/2/22 - Broad Arrow announces its inaugural live auction event, set to take place during Monterey Car Week.

8/10/22 - Hagerty announces it has entered into a Definitive Agreement to acquire all outstanding shares of Broad Arrow in a transaction valuing Broad Arrow at $108.0 million in the aggregate. Additional color from HGTY’s 2022 Q2 Investor Presentation:

“[B]usiness ramping up faster than anticipated due to strong execution and synergies from the strength of the Hagerty brand and platform.”

“Proven leadership team with a strong cultural fit.”

“Expected to be immediately accretive in 2022.”

I am quite skeptical of this claim!

“The deal structure incentivizes, and aligns, the team over a five-year period through an all-stock transaction for the remaining 60% valued at $64.8 million.”

Broad Arrow has an upcoming auction of roughly 300 collector car lots set for mid-November 2022 in West Palm Beach, Florida; I am told that they will need a minimum of 600 bidders to ensure viability. I understand that Broad Arrow / Hagerty have something on the order of 100 bidders registered to date; only 500 to go over the next month!

The details of the analysis are beyond me. As a layperson, the deal(s) seem by turns suspect if not illegal but for the fact that the DoJ doesn't give a shit about anti-trust anymore, woefully undervalued, and occasionally overvalued. It also seems like some youngster told them about a guy who made a lot of money on this "youtube" website and they should really look into it but they don't seem to have any idea what to do with it. On the one hand, in fairness to them, it seems to be very difficult to make a good car themed show, as the graveyard of Top Gear spin-offs and imitators can attest; on the other hand, if they were savvy car people they would have known that.

Interesting viewpoint.

I’ve spent a good amount of time researching the business and come away with a different conclusion. The Broad Arrow acquisition should be immediately accretive in 2022, based on the estimated revenues generated from their first 2 auctions and the upcoming West Palm Beach auction in November:

Monterey Jet Center Auction (August 18, 2022)

-Total Sales: $55.3M

-Estimated premiums to Broad Arrow: $5.3M

-Registered Bidders: unknown

Jim Taylor Collection (October 14-15, 2022)

-Total Sales: $21.3M

-Estimated premiums to Broad Arrow: $2.2M

-Registered Bidders: 1,000+

West Palm Beach Auction (November 18-19, 2022)

-TBD

It’s important to note that the estimated premiums earned by Broad Arrow listed above are only the buyer premiums. Assuming that seller premiums were 5-7% of the hammer price, there would be an additional $3.4M - $4.8M in premiums earned by Broad Arrow. Given that the physical auction space is generally the largest expense, and both completed auctions were at locations either already being used by Hagerty or hosted by the collector himself. Similar live-auction car events produce EBIT margins of 40% - 50% even when they are paying for the venue, so it’s highly likely that these events will be accretive to Hagerty’s operating profit this year.

Looking ahead for the live-auction business, it’s pretty clear that each of Hagerty’s main car show events will ultimately host a Broad Arrow auction. With the potential for 5-7 live-auctions per year in the near term and standard margin profiles, it doesn’t seem crazy that Broad Arrow’s live-auction business can be generating $250M - $350M in total auction sales, which would equate to $25M - $30M in revenue/$12M - $18M in EBIT. While that alone makes the $108M purchase price of Broad Arrow (which is leading the marketplace business for Hagerty) seem reasonable, it doesn’t even touch what the real opportunity here is…an online auction similar to Bring-A-Trailer.

On October 17th, Hagerty announced the upcoming November launch of online auctions through Hagerty Marketplace. It’s difficult to nail down exact numbers, but there are an estimated $50B of classic/collector vehicle transactions taking place each year and Hagerty saw $12B of transactions occur just within its own membership base over the last 12 months. Bring-A-Trailer grew its auction value sales from ~$400M in 2020 to an estimated $1.4B for 2022 and there is no reason that Hagerty’s upcoming offering can’t replicate that success. In fact, it appears that Hagerty’s online auctions will have superior features that facilitate trust in the transaction, increasing buyer confidence in the vehicle they are bidding on. From a business standpoint, similar online auction platforms earn 60% - 80% EBIT margins. With a 7% take rate on the hammer price and similar margin profiles, even capturing 10% of the transactions within its membership base would result in $84M in incremental revenue and $50M - $67M of increment EBIT.

Every piece of Hagerty’s business fits together into a synergistic flywheel. The marketplace business provides another low-cost customer acquisition platform for its core insurance business, which already has a CAC that is 1/2 the industry average. Every event and online platform that Hagerty owns is a low-cost, hard to replicate advertising channel that can be leveraged in numerous ways. Each new insurance policy is an additional opportunity to attach Hagerty Drivers Club, which has had a 75% attach rate over the last few years. The marketplace platform will only further drive new data into their Valuation Tool, which itself has potential for interesting monetization paths (think Moody’s bond ratings but for cars). Speed Digital brings real-time inventory from more than 200 dealers that managed 8,200 collector cars in inventory for sale at the time Hagerty acquired the company.

The flywheel continues to turn.